CHARLOTTESVILLE PARKING ANALYSIS - DRAFT

City of Charlottesville

Nelson\Nygaard Consulting Associates Inc. | i

CHARLOTTESVILLE PARKING ANALYSIS - DRAFT

City of Charlottesville

TABLE OF CONTENTS

Page

Summary of Needs and Recommendations 6

University Corner On-street Parking Inventory 18

On-Street Parking Restriction Glossary 19

Off-Street Parking Utilization 24

General Public Parking Survey 48

Business Owner Parking Survey 55

PARKING and TDM RECOMMENDATIONS 60

Offer Viable and Attractive Commute and access Alternatives 68

Maintain (and monitor) Current Parking Supply 70

Special Project Area Recommendations 71

TABLE OF FIGURES

Page

Figure 1 Downtown Study Area 10

Figure 2 University Corner Study Area 11

Figure 3 Total Parking Inventory – Downtown Study Area 13

Figure 4 Public Parking Inventory – Downtown Study Area 14

Figure 5 Downtown Study Area Parking Inventory 16

Figure 6 Downtown On-Street Parking Overview 17

Figure 7 On-Street Parking Inventory – University Study Area 18

Figure 8 University Corner Study Area Parking Inventory 18

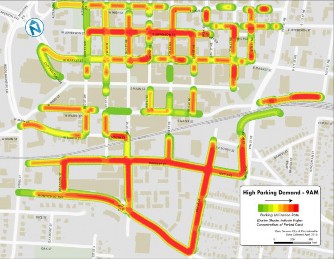

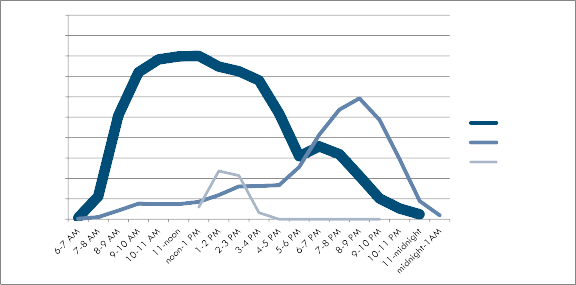

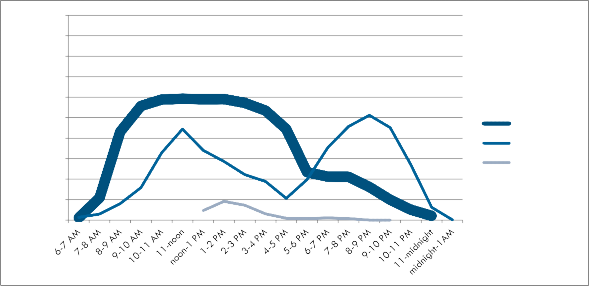

Figure 9 Downtown Parking Demand 9 AM 22

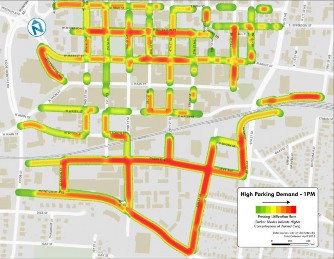

Figure 10 Downtown Parking Demand 1 PM 22

Figure 11 Downtown Parking Demand 6 PM 22

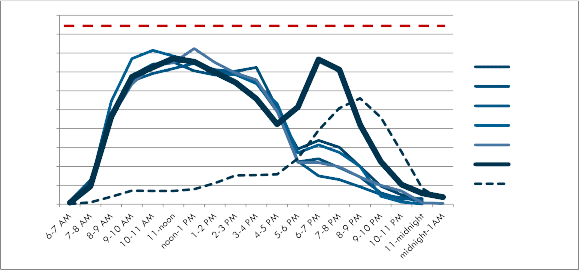

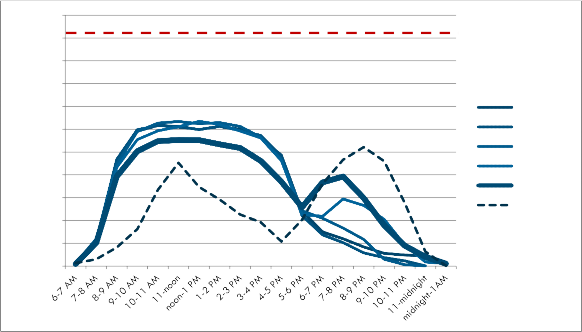

Figure 12 University Parking Demand 9 AM 23

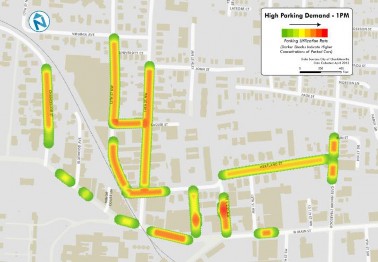

Figure 13 University Parking Demand 1 PM 23

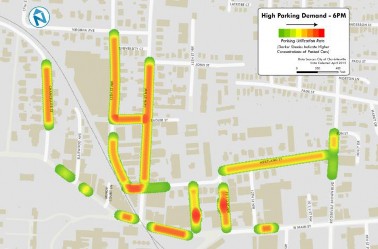

Figure 14 University Parking Demand 6 PM 23

Figure 15 Market Street Garage 24

Figure 16 Water Street Parking Garage 25

Figure 17 Downtown Cultural Zone Weekday Utilization Table 28

Figure 18 Downtown Cultural Zone Weekday Turnover Table 28

Figure 19 Downtown Cultural Zone Saturday Utilization Table 30

Figure 20 Downtown Cultural Zone Saturday Turnover Table 30

Figure 21 Downtown Government Zone Weekday Utilization Table 32

Figure 22 Downtown Government Zone Weekday Turnover Table 32

Figure 23 Downtown Government Zone Saturday Utilization Table 33

Figure 24 Downtown Government Zone Saturday Turnover Table 34

Figure 25 Downtown Market Zone Weekday Utilization Table 35

Figure 26 Downtown Market Zone Weekday Turnover Table 36

Figure 27 Downtown Market Zone Saturday Utilization Table 37

Figure 28 Downtown Market Zone Saturday Turnover Table 37

Figure 29 Downtown Southeast Zone Weekday Utilization Table 39

Figure 30 Downtown Southeast Zone Weekday Turnover Table 40

Figure 31 Downtown Southeast Zone Saturday Utilization Table 41

Figure 32 Downtown Southeast Zone Saturday Turnover Table 41

Figure 33 University Zone Weekday Utilization Table 43

Figure 34 University Zone Weekday Turnover Table 43

Figure 35 University Zone Saturday Utilization Table 44

Figure 36 University Zone Saturday Turnover Table 45

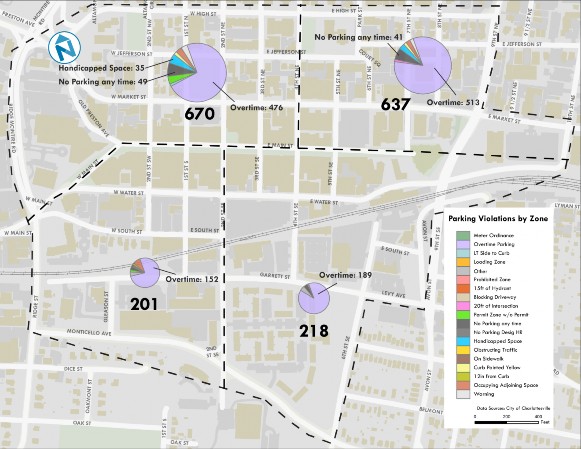

Figure 37 Parking Violation January - March 2015 45

Figure 38 Downtown Parking Violations by Zone (January to March 2015) 46

Figure 39 University Corner Parking Violations (January to March 2015) 47

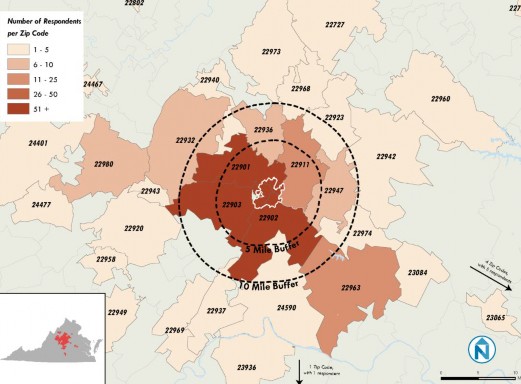

Figure 40 Home Zip Code of Survey Respondents 49

Figure 41 General Public Length of Time to Find Parking 50

Figure 42 General Public Maximum Willingness to Pay 51

Figure 43 Home Zip Code of Downtown Employees Surveyed 52

Figure 44 Workforce Commute Mode Share 53

Figure 45 Survey Response by Type of Business 55

Figure 46 Busy or Very Busy Downtown Business Hours 56

Figure 47 Employer Suggestions to Improve Employee Parking 57

Figure 48 Employer Perceptions of Customer Parking Concerns 58

Figure 49 Critical Parking Factors for Customers 59

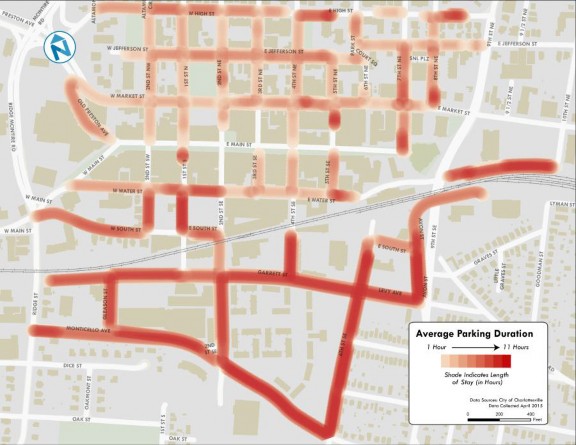

Figure 50 Average Downtown Parking Duration 62

Figure 51 Average University Corner Parking Duration 63

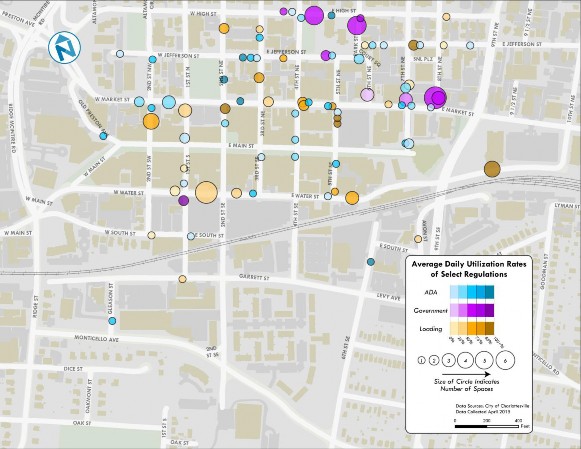

Figure 52 Average Daily Utilization Rates of Parking Regulations 64

Figure 53 SFPark Mobile App 65

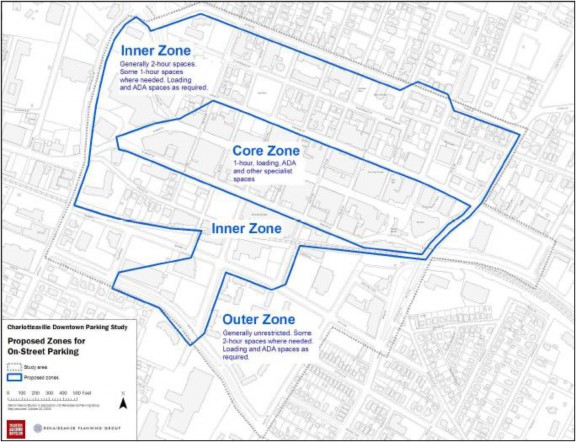

Figure 54 Zone Definition (2008 Report) 66

Figure 55 Courthouse Parking Profile 71

The City of Charlottesville completed a Downtown Parking Study in 2008, which examined the adequacy of parking availability, the existing designation and allocation of parking spaces, and strategies for parking management. The study made four broad recommendations:

Simplify parking management to reflect three broad areas of unique demand patterns: the Core Zone immediately abutting the pedestrian mall which should be prioritized for loading, ADA access, and very short term parking; the Inner Zone encircling the Core that should be prioritized for visitors and short term parkers; and the Outer Zone to accommodate longer duration parking needs.

Create a City Parking Department to more holistically manage parking.

Replace the Parking Exempt Zone (PEZ) with minimum parking requirements and/or an in lieu payment option in order to ensure new development would not overwhelm existing supply.

Encourage employers to participate in transportation demand management strategies and explore the creation of a parking benefit district.

Although some of the recommendations of the 2008 study have been implemented – most notably the tailoring of curbside regulations to reflect the diverse zones and the restoration of parking minimums - public parking remains an issue in downtown Charlottesville. In fact, the 2014 National Citizen Survey Community Livability Report for Charlottesville recorded that 24 percent of respondents consider traffic, parking, and public transportation to be the single biggest issue facing the community. Public parking received only a 21 percent approval rating in that same report.1

The purpose of this study was to update and reassess the recommendations of the 2008 study and recommend a course of action to improve parking and access to support a vibrant and vital downtown for the diverse range of workers, visitors, and patrons in the city. The study was a data-

![]()

1 Community Livability Report for Charlottesville, Virginia (The National Citizen Survey, 2014)

driven process to identify opportunities for change, innovative alternative management, and pathways to accommodate existing development and future growth. The findings of this effort, in tandem with those produced by the 2014 West Main Street Parking Opportunities and Analysis, yield a complete picture of parking conditions and opportunities along the entirety of Charlottesville’s major commercial, educational, and mobility core.

The following report, focusing on both the historic downtown and university-adjacent neighborhoods, reviews existing parking supply and demand, analyzes key trends, addresses stakeholder issues, presents parking policy and demand management options, and makes specific recommendations for action in the short- and long-term.

SUMMARY OF NEEDS AND RECOMMENDATIONS

The study team gathered information from a variety of sources in order to identify the underlying needs facing Charlottesville that parking management must seek to address:

Parking and access for downtown workers. Many downtown employees drive to work and many of them cannot afford the price to park daily in one of the off street facilities. A significant portion of downtown workers can and would commute via an alternate mode if it were convenient and compelling to do so. When they must drive and park, however, workers need affordable accommodation that does not require the “2-hour shuffle.”

Available parking for commercial patrons. Charlottesville is a destination. Continued strength of the commercial establishments and entertainment venues means that parking must be easy to access, reliably available, and convenient to use for visitors and patrons.

Accommodation of court functions. As a municipality and county seat, Charlottesville sees a dramatic rise in parking demand on court days. Charlottesville must have ready solutions to address court needs to efficiently serve this judiciary function.

Maintenance of neighborhood quality of life. Charlottesville is a living downtown. Residents live above and adjacent to shops and commercial destinations. While strong commercial support is required, parking management must also be cognizant of neighborhood quality of life and minimize spill over parking pressures.

Access and circulation. Parking is only part of the downtown picture. Curbsides are also needed to drop off patrons, students or other passengers; short term loading and deliveries; and efficient circulation in the downtown that minimizes congestion and other negative environmental, economic and community effects.

Accommodation of growth and change. Charlottesville is fortunate to remain a growing economy. However, in some instances, growth means the conversion of existing parking resources. The city must plan to manage and meet parking, access and circulation demand that accompanies this new growth and adapts to changing resource supply.

Efficient and coordinated management of resources. Charlottesville must optimize resources to make parking and access convenient, efficient and understandable.

After thoroughly reviewing available data and gaining insight from a diversity of users and stakeholders, the study team recommends the following summarized actions to address the above stated needs. These can generally be grouped into three broad strategies:

At present the city is not optimizing the parking resources that it has. This creates a somewhat artificial sense of parking shortage. While some parking resources are over-subscribed, others demonstrate available capacity that could be better used.

Establish a City Parking Department. As in 2008, a City Parking Department remains necessary in order to more holistically and responsively manage parking to the benefit of businesses, visitors, and residents.

Adopt demand-responsive management for both on- and off-street parking resources. Demand is different and uneven throughout the downtown. There are demands for short term and long term parking that are currently not well matched to the resources. In general, on-street parking is the best resource to serve short term parking needs while off-street parking is better suited to longer-term parkers. Pricing structures help to sort users to the optimal resource. Recommended demand responsive strategies are to:

Meter the Highest Demand On-Street Parking. This generally applies to the core of the downtown and main commercial corridor of University Corner.

Right-size Off-Street Parking Fees. In general, on-street parking is more desirable than off-street parking thus demand responsive pricing would indicate that off-street parking fees should be lower than on-street rates.

Maintain some free parking. Several areas of downtown have comparatively low demand for parking and should, at present, remain a free parking resource.

Revisit Regulations. Consider removing or relieving time limits on parking, especially in areas where meters will be adopted. Align times and durations of regulations with periods of demand. Re-examine areas of special reservation of curbsides for where these uses can be better served in off street locations or through new management strategies.

Make Parking Easy. Utilize available parking technologies to make parking easy including finding available spaces, extending time remotely, and permitting payment via a variety of mechanisms.

Improve and equalize enforcement. Management strategies, and the establishment of a new department, should facilitate enforcement across all zones.

Create Parking Benefit District(s). Similar to recommendations from 2008, parking revenues should be dedicated to one or more parking benefit districts to support parking facilities and management, arrange shared parking, improve information, and implement transportation demand management.

Most people make rational choices in how they travel. If driving and parking is cheap and convenient and other modes of travel cost more in both time and money, people will generally choose to drive even when other viable options are available. People generally respond positively to “carrots.” Transportation Demand Management offers information and incentives that help make alternatives to driving and parking rational choices for users.

Design and Implement a Transportation Demand Management Program / establish a Transportation Management Association. Transportation demand management programs provide support and incentives to enable and encourage arrival

downtown by means other than single occupancy vehicles. These options provide relief to stresses on the parking system and serve employers, employees, and visitors alike.

Transportation management associations help to develop, promote, and tailor such services to the downtown and University Corner audience. The Parking Department could, more broadly, be referred to as a “Mobility” Department to ensure that promotion of a broad range of access to the downtown and across the city were also part of the charge of this new department.

Enable, promote, and encourage the continued expansion of alternative mobility options. As each new mobility options appears, the set of methods employed to slow or reverse parking demand becomes larger. These may include the addition of

low-stress bicycle facilities and adequate bicycle parking, enhanced transit operations and services, bicycle and car sharing systems, and other similar services.

Better management of existing on and off street parking resources will significantly reduce the parking pressures and better match users to the resource best suited to their needs. Strong promotion of TDM efforts and continued enhancement of alternative travel options will serve Charlottesville well in maintaining its reputation and charm as an attractive, livable and sustainable city. But demand for parking will remain. As a small and growing city in a relatively rural region, access by automobile will continue to be an important mode of access. Current parking levels should be maintained, but continuously monitored and evaluated.

Maintain existing parking requirements for new development. With the elimination of the parking exempt zone, new developments will largely meet their own new parking demands; therefore future parking demand is not anticipated to outpace added supply. Similarly the current “in lieu” payment option should remain for those properties unable to provide parking on site or desiring to participate in a shared arrangement.

Strategically expand where opportunities present themselves

Partner in parking replacement or enhancement. The city is growing. As development occurs the city will see a temporary, and in some cases permanent, reduction in the number of public or employee parking spaces in the downtown. The city should partner with private owners to optimize opportunities to replace this parking supply and where prudent, enhance it.

Engage in shared parking arrangements. As was observed in 2008, there are surplus off-street parking spaces downtown, however many of these empty spaces are not available to the general public. Shared parking arrangements to make use of existing underutilized spaces can help address unmet parking demand.

Participate in development. As new developments occur downtown, the city may wish to partner with developments to integrate new public parking spaces into development projects to replace lost parking or sensitively augment supply and better distributing parking options throughout the downtown. The need for additional supply should be judiciously monitored and can only be correctly evaluated after effective parking and demand management programs have been implemented.

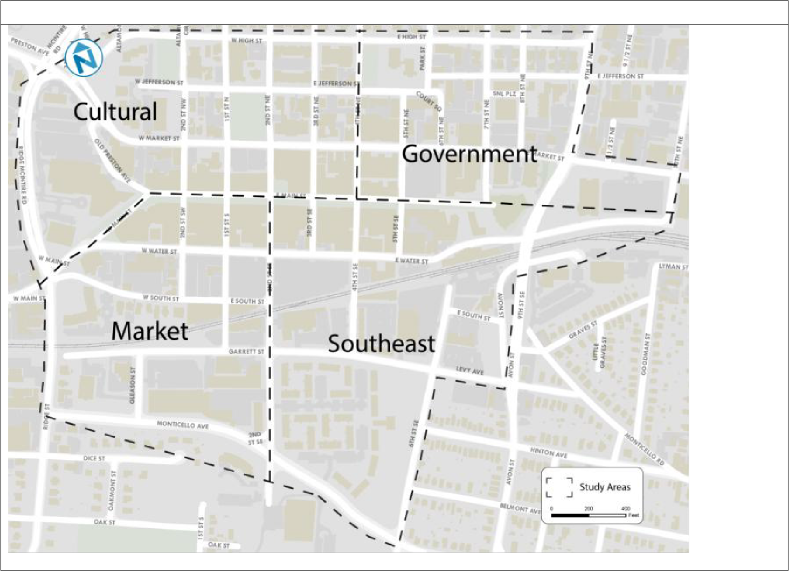

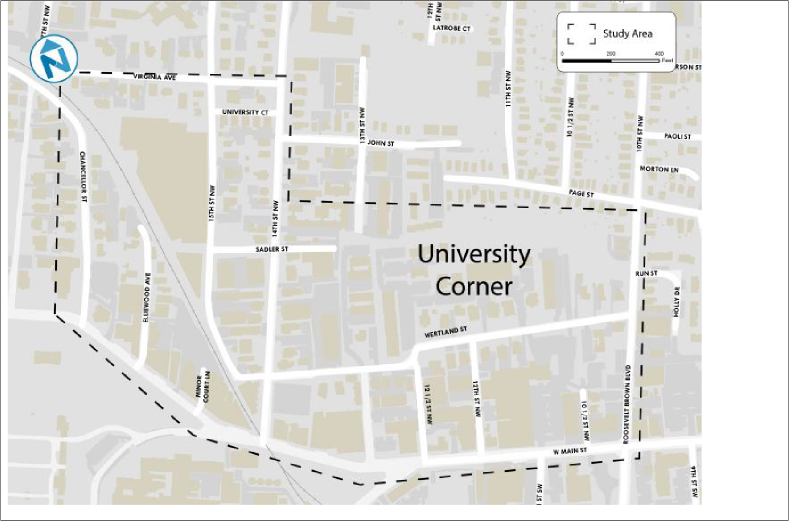

The study area concentrated on Downtown and University Corner (The Corner). Downtown encompasses a roughly 60 block area generally bounded by High Street, 6th and 9th streets, Monticello Avenue, and Ridge McIntire Road (Figure 1). University Corner includes roughly 20 blocks bounded by Virginia Avenue, 14th Street, Wertland Street, 10th Street NW, West Main Street, and Chancellor Street (Figure 2). The West Main Street corridor, studied in 2014, bridges the two areas.

For the purposes of this analysis, the Downtown study area was subdivided into four study zones, each with unique on-street supply and demand characteristics:

Cultural Zone

Containing the Paramount Theater, the Jefferson-Madison Regional Library, the McGuffey Art Center, and public parks

North of the Main Street Pedestrian Mall and west of 4th Street NE

Government Zone

Containing City Hall, the Albemarle County Circuit Court, and Sheriff’s Office

North of Main Street and east of 4th Street NE

Market Zone

Containing Charlottesville City Market and the Main Street Arena Event Center

South of Main Street and west of 2nd Street SE

Southeast Zone

South of Main Street and east of 2nd Street SE

The Downtown study area is co-terminus with the 2008 study area to enable crosswise comparison between data and findings. It includes the city’s largest concentration of office, municipal service, dining and retail uses, in addition to a fair concentration of downtown residences. The University Corner area primarily consists of University-oriented commercial uses and a significant amount of residential units, many occupied by students and other university affiliates.

CHARLOTTESVILLE PARKING ANALYSIS - DRAFT

City of Charlottesville

CHARLOTTESVILLE PARKING ANALYSIS FINAL REPORT

City of Charlottesville

Figure 2 University Corner Study Area

CHARLOTTESVILLE PARKING ANALYSIS - DRAFT

City of Charlottesville

The project gathered an extensive amount of detailed information in order to understand parking conditions in the city center and University Corner areas. This information:

Provided a spatial understanding of parking supply, pricing, and restrictions

Identified typical occupancy and accompanying issues

Informed an appropriate set of prospective management techniques

Identified and engaged affected stakeholder groups

Provided insights into prevailing attitudes towards potential solutions

The data reflecting this subject matter was collected through several initiatives, including:

Parking Inventory, Utilization, and Turnover Assessment. Inventory data was collected in April 2015 including the number of on- and off-street spaces and their corresponding regulations or management practices. A comprehensive on-street occupancy survey was undertaken in stages beginning Wednesday, April 22, 2015 and ending May 2. Weekday data was collected in hourly cycles from 8 a.m. to 8 p.m. while Saturday data collection extended from 11 a.m. to 10 p.m. The survey dates were chosen such that the demand impact of the University of Virginia would be reflected in the count while avoiding confounding issues of major festivals, holidays or events. Private and public off-street lot utilization was determined on Wednesday, May 13, 2015 from 7 a.m. to 9 p.m. and Saturday, May 16, 2015 from 10 a.m. to 10 p.m.

Integration of Municipal Data. Data collected by the City of Charlottesville pertaining to municipal parking structure utilization and ticketed parking violations was provided to Nelson\Nygaard for use in this analysis. Data from Thursday April 23, 2015 and Saturday April 25, 2015 was chosen for use in the study.

Stakeholder Meetings. On March 31st and April 1st 2015, Nelson\Nygaard conducted stakeholder meetings at Charlottesville City Hall. Stakeholders were divided into focus groups based on affiliation. Groups of city residents, major employers, small business representatives, and governmental agency staff met with facilitators to discuss issues pertinent to each group.

User Surveys. Throughout April and May 2015, three online surveys collected qualitative data on user experiences, preferences, and perceptions. Each survey targeted a different segment of the downtown Charlottesville user population: business operators, workers, and the general public. The surveys informed development of context-specific and effective management strategies.

A comprehensive parking inventory of all on-street spaces was performed for the Downtown and University Corner study areas. In the downtown, municipal garages and all off-street surface lots containing 20 or more parking spaces (public and private) were also inventoried.

Allowing for variation due to temporary construction activities, there are approximately 4,280 parking spaces accessible to the public in the Downtown study area. This number differs significantly from the 6,000 reported in the 2008 study as it does not include the over 1,700 parking spaces located in private parking structures inaccessible to the public. For example, the garages at Merkle | RKG at 701 Water Street East and indoor/underground parking for the ACAC Fitness & Wellness Center located at 455 2nd Street SE were not included. The Omni Hotel at 212 Ridge McIntire Road has about 400 parking spaces in a large private garage. While the garage is primarily for guests, the hotel has monthly passes available for $125/month and hourly parking for $2/hour when there is space available. There are approximately 90 people with monthly parking permits.

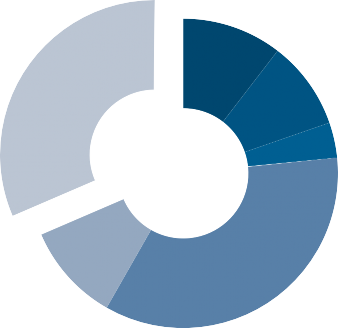

Figure 3 Total Parking Inventory – Downtown Study Area

1,347

Private Surface Lot Spaces

1,932

Public Off-Street Spaces

1,001

Public On-Street Spaces

Of the 1,347 private surface lot parking spaces, some parcels currently available as parking are proposed for future development. These include 63 parking spaces located in a gravel parking lot at First Street South and Garrett Street. At 201 Monticello Avenue, a former church building provides 50 parking spaces until construction begins for its approved redevelopment. Finally, the block bounded by Water Street, 1st Street, South Street and 2nd Street SW may be developed in the future. The property currently accommodates 105 public spaces and 23 private. These planned redevelopments result in an anticipated reduction of parking supply by roughly 220 spaces (about 5 percent).

On-Street

Of the 1,001 on-street parking spaces in the Downtown study area, 447 are reserved for short- term parking restricted by time limits (45 percent of the on-street supply). There are 396 unrestricted spaces (40 percent), allowing for all-day parking. Finally, 127 spaces (13 percent) are designated for special uses such as loading zones, handicapped spaces, and permit holders, including 31 reserved for government staff (Figure 4). All on-street parking in the City of Charlottesville is currently unpaid.

![]()

Off-Street

Of the off-street public parking inventory, all of which is paid parking, the two municipal parking structures account for 77

percent of supply (1,492

Figure 4 Public Parking Inventory – Downtown Study Area

Time Restricted On-Street Spaces

spaces). The Market Street garage has 473 spaces and the Water Street garage has

Private

Surface Lots

15% Unrestricted

On-Street

Spaces 14%

1,019. Parking garages operate daily from 6 a.m. to midnight with extended hours (to 1 a.m.) on weekends. Sunday hours are noon to 10 p.m.

The cost to park at the

Public Paid Off-Street

Public Parking

On-Street Special Uses 5%

Market Street garage is $1.25 for the first half hour and

$2.50 for any hour thereafter with a daily maximum of

$20.00. The Water Street garage is $2.00 per hour, or

Lots

15%

Structures 51%

any portion thereof, with a daily maximum fee of $16.00.

Pre-paid monthly permit parking is $135 at the Market Street garage and $120 at the Water Street garage. The Market Street garage has 381 monthly parking permits and 87 people currently on a waiting list. As of July, 2015, the Water Street garage has 900 monthly contracts in place and an additional 106 spaces leased by a private 3rd party company. Monthly permits no longer remain available for the Water Street garage and a waiting list has been instituted.

The garages offer a parking validation program for area businesses. Roughly 150 downtown businesses participate in the validation program providing one or two hours of free parking to their customers. Businesses pay a discounted fee to the Charlottesville Parking Center, the operator of the garages, to provide patrons or visitors validated parking.

The remaining 23 percent of off-street publicly available parking supply (344 weekday daytime spaces, 440 nights and weekends) is located in surface lots at 100 East Market Street, 100 Water Street East, and 100 South Street West (Figure 5). The Citizens Commonwealth Center at 300 Preston Avenue contributes 96 spaces to the public supply outside of regular business hours.

Effects of Development/Projects on Off-Street Supply

Three foreseen projects will have an effect on the overall downtown parking supply. The Levy Lot, located on Market Street between 7th and 8th Streets NE is slated for redevelopment by the housing authority. This lot is currently used for city employee parking and provides 63 private off-street spaces (permit required, no daily sale of parking to the public) in the Government Zone.

A reconstruction of the Belmont Bridge carrying 9th Street SE over the railroad will remove approximately 50 unregulated parking spaces beneath one of its spans. This lot was outside of the study boundaries and not included in the off-street inventory of this study, however it is important to note the pending loss of these spaces.

Finally, the Market Plaza proposal will replace and redevelop the existing parking lot at Water and First Streets. After a three year disruption, 102 of the existing 105 public parking spaces will be restored. The City Market will continue to operate on Saturday mornings in the only remaining publicly available surface lot in the Market Zone until the development is completed.

CHARLOTTESVILLE PARKING ANALYSIS - DRAFT

City of Charlottesville

Figure 5 Downtown Study Area Parking Inventory

Nelson\Nygaard Consulting Associates Inc. | 16

CHARLOTTESVILLE PARKING ANALYSIS - DRAFT

City of Charlottesville

The on-street parking supply in the Downtown study area is categorized by a number of timed regulations (two hour, one hour, 15 minutes), special uses (loading, dropoff, ADA, government, permit, motorcycle), and unrestricted spaces (See: Glossary, Pages 18-19).

Figure 6 Downtown On-Street Parking Overview

Downtown Study Area On-Street Parking Overview | ||||

Cultural Zone | Government Zone | Market Zone | Southeast Zone | |

Unrestricted | 27 | 10 | 82 | 278 |

2 hour | 145 | 117 | 100 | 54 |

1hour | 7 | 17 | 7 | 0 |

15 minutes | 0 | 0 | 3 | 0 |

ADA | 19 | 22 | 3 | 6 |

Loading | 17 | 14 | 11 | 11 |

Government | 1 | 28 | 2 | 0 |

Permit | 0 | 0 | 9 | 4 |

Dropoff | 3 | 0 | 0 | 0 |

Motorcycle | 0 | 0 | 1 | 1 |

Note that the figures given are weekday figures determined in April 2015. Inventory may fluctuate due to temporary events or construction activity. For example, seven two-hour spaces found on Market Street between 2nd and 3rd Streets NE can be converted into a loading zone for the Paramount Theatre through the use of hinged restriction signage. These spaces are included in the time restricted parking supply.

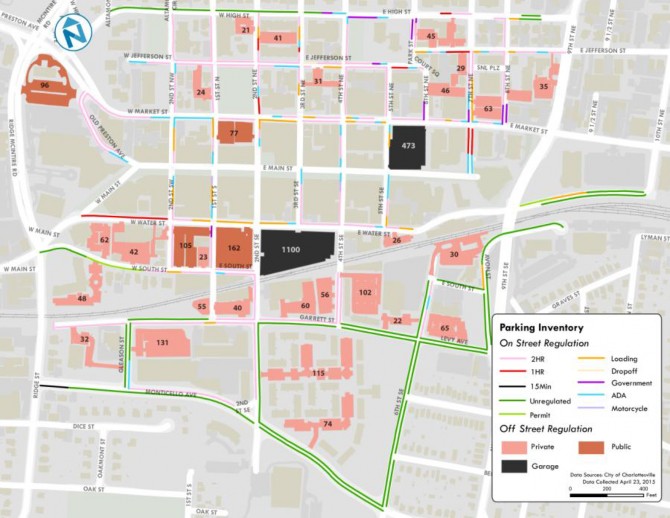

UNIVERSITY CORNER ON-STREET PARKING INVENTORY

Again allowing for temporary variation, there are 196 on- street parking spaces in the University Corner study area.

Represented graphically in

![]()

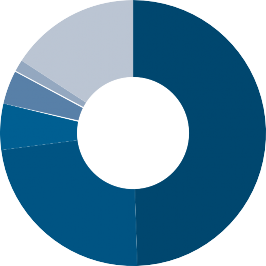

Figure 7 On-Street Parking Inventory – University Study Area

Figures 7 and 8, roughly half of these spaces (97) are unrestricted while 57 spaces (29 percent) have some time

limit. There is a significant

ADA 2%

Loading 4%

Residential

Permit 16%

amount of residential permit parking in this area. Thirty- one spaces (16 percent of

curbside spaces), all found

15 Minute

6%

Unrestricted 49%

along Wertland Street, require a Zone 1 permit between the hours of midnight and 7 p.m., seven days per week.

Two Hour

Limit 23%

Figure 8 University Corner Study Area Parking Inventory

Charlottesville is recognized as a Silver Bike Community by the League of American Bicyclists and a Gold Walk Community by the Pedestrian and Bicycle Information Center. As of February 2015, the city had 13.6 miles of signed bicycle routes, 13.1 miles of bicycle lanes, 3.3 miles of shared lane markings, 9.6 miles of shared use paths, and 0.4 miles of contraflow bike lanes (located on South Street, at the western edge of the study area). U.S. Bike Route 76, an east-west bike route that runs from Nelson County through Charlottesville to Fluvanna County passes south of the Downtown Mall on Water Street.2

There are currently 26 bicycle parking facilities downtown that can accommodate a total of 160 bikes. Currently, downtown bike facilities are predominantly “staple” and bollard styles, along with two bike corrals (18 total spaces). The Market Street Parking garage offers 30 short-term bike parking spaces.

The city’s Bicycle/Pedestrian Master Plan was updated in 2015 and contains specific recommendations for city policies and transportation facilities. To help identify where bicycle and pedestrian facilities are most needed, the City measured demand for walking and biking and found the Downtown Mall and the University of Virginia to be two clear areas where bicycle and pedestrian demand are highest.

The city’s Bicycle/Pedestrian Master Plan recommends bicycle lanes for West Main Street, Ridge McIntire Road, and 9th Street NE, while climbing bike lanes are prioritized for East/West High Street, West Market Street, and Monticello Avenue. North of the study area shared roadways are recommended on Park Street.

Finally, the plan notes that as the City of Charlottesville reviews and revises the sections of City code that address parking, it should adopt bicycle parking standards. The new standards should address different types of bicycle parking for different needs, including long-term versus short term storage, as well as protection from the elements.

ON-STREET PARKING RESTRICTION GLOSSARY

Two Hour – Parking limited to a duration of two hours between 8AM and 6PM, Monday through Saturday. These spaces may defer to loading zone or trash pickup restrictions during certain morning hours as is common along Water Street.

One Hour – Parking limited to a duration of one hour between 8AM and 6PM, Monday through Saturday.

Fifteen Minutes – Parking limited to a duration of fifteen minutes. Times of day that this restriction is in effect vary between downtown and the University Corner. May share restriction with loading zones.

Permit – Parking restricted to those with corresponding parking permits. These are most often permits for residents which apply to a specific zone. These spaces are not time-limited.

![]()

2 http://tjpdc.org/route76/albemarlemap.html

Government – Parking reserved for governmental functions. Examples include but are not limited to Sheriff Department vehicles, judges’ personal vehicles, and vehicles owned by the Department of Social Services. These spaces are not time-limited.

Loading Zone – Temporary parking for commercial vehicles involved in delivery of goods and services. Restriction time of day varies and is sometimes shared with two hour parking. When signed expressly as a loading zone, this restriction is in effect between 8AM and 6PM, Monday through Saturday. These spaces are not time-limited.

ADA – Parking reserved for persons with disabilities. Vehicles must display either a state-issued handicapped license plate or a hanging placard behind the front windshield. These spaces are not time-limited.

Drop-off – Temporary standing space for convenient drop-off of passengers. This restriction is generally associated with churches in the cultural zone and is often only in effect on Sundays.

Motorcycle – Parking reserved for multiple motorcycles in the size of a traditional parking space. These spaces are not time-limited.

Unrestricted – Unreserved and unsigned on-street parking with no time limit.

Based on the parking data collected, the following metrics were calculated and analyzed for various subsets of parking:

Downtown and University Corner on-street average hourly utilization

Downtown and University Corner on-street average duration

Downtown and University Corner on-street average turnover

Downtown off-street periodic utilization

Downtown parking structure hourly utilization

Parking utilization is defined as a ratio of occupied parking spaces divided by the total inventory. Utilization rates directly reflect the ability of a motorist to find convenient and available parking within a particular area. Rates between 75 and 85 percent signify a nearing of the practical capacity for on-street parking; the opportunity to find parking is reasonable and turnover rates remain healthy. Exceeding the 85 percent threshold on-street can result in undesirable consequences from convenience, traffic generation, and commercial perspectives. Below 95 percent utilization is typically desired for off-street parking facilities where parking can be more predictably managed. Exceeding these levels can mean that customers will have difficulty finding parking on a particular street, group of streets, or within a facility. A utilization rate greater than 100 percent describes an overcrowded parking condition and implies the likely presence of illegal parking.

Duration describes the length of stay of a single vehicle in a particular parking space. If all regulations are being followed, the observed duration is equal or less than the posted time limit (where applicable). The typical parking time limit in Charlottesville is two hours. Time limits are employed as a strategy to encourage turnover of prime parking spaces, and maximize the number of individuals who can use a particular space during business hours.

Turnover, directly related to duration, calculates the number of vehicles that use a parking space over a study period. The average turnover metric measures the performance of groups of parking spaces with respect to serving potential customers/visitors. When restrictions are present, turnover should approach or exceed the length of the study period divided by the time limit of the restriction. For example, a two-hour space during a 10-hour study period should handle a minimum of five vehicles.

Overall, parking demand is substantial, but uneven, across the Downtown and University Corner areas. Each zone demonstrates unique parking behavior that reflects the dominant land uses and generators in each area. Generally off-street parking is less well utilized than on-street parking. This reflects expected economic behavior given that one must pay to park off street while parking on street is free. Demand also differs by the time of day as shown in Figure 9 through Figure 14.

CHARLOTTESVILLE PARKING ANALYSIS - DRAFT

City of Charlottesville

Figure 9 Downtown Parking Demand 9 AM Figure 10 Downtown Parking Demand 1 PM

Figure 11 Downtown Parking Demand 6 PM

CHARLOTTESVILLE PARKING ANALYSIS FINAL REPORT

City of Charlottesville

Figure 12 University Parking Demand 9 AM Figure 13 University Parking Demand 1 PM

Figure 14 University Parking Demand 6 PM

CHARLOTTESVILLE PARKING ANALYSIS - DRAFT

City of Charlottesville

OFF-STREET PARKING UTILIZATION

Charlottesville has two primary public parking facilities, both located in the Downtown area. The 473 space Market Street parking garage is located on the north side of the Mall toward the east end adjacent to City Hall and proximate to the court complex and Pavilion – each about one block away. The 1019 Water Street parking garage is centrally located one block south of the Mall.

Figure 15 Market Street Garage

100%

90%

80%

Utilization Rate

70%

60%

50%

40%

30%

20%

10%

0%

Weekday Avg Saturday Sunday

500

450

400

Parked Vehicles

350

300

250

200

150

100

50

0

473 total spaces

Weekday Monday Tuesday Wednesday Thursday Friday Saturday Sunday

Source: Charlottesville Parking Center data for the week of April 20, 2015

Both garages see substantial demand on Saturday evenings, although neither exceeded 60% occupancy on the sample Saturday. The Water Street Parking Garage also saw significant demand during the market period (around noon).

Figure 16 Water Street Parking Garage

100%

90%

80%

Utilization Rate

70%

60%

50%

40%

30%

20%

10%

0%

Weekday Avg Saturday Sunday

1100

1000

1019 total spaces

900

800

Parked Vehicles

700

600

500

400

300

200

100

Monday Tuesday Wednesday Thursday Friday Saturday Sunday

0

Source: Charlottesville Parking Center data for the week of April 20, 2015

Both garages have issued a large quantity of monthly parking permits. At the time of data collection (April 2015), Market Street had issued 381 monthly permits while Water Street had issued 842 (plus another 106 3rd party reserved spaces). If all monthly parkers appeared demanding spots at the same time, this would consume 80% and 93% of the garage spaces respectively. However, this does not happen. In actuality, monthly permit holders represent roughly one-half (50%) of vehicles utilizing the garages with transient (daily) parkers making up the balance. Fewer than 250 monthly permit holders routinely occupy the Market Street garage while no more than 545 of the Water Street permit holders occupied the garage at any given time.

Only about 65% of permit holders use their permits on a given day. It is common practice to “oversell” permits at a rate of 10% to 25% (15% is a common benchmark industy standard), however Charlottesville is demonstrating the ability to comfortably oversell by 25% or more.

The extensive wait list for monthly permits in the Market Street garage (87 at present) and the high relative oversell rate indicate that price is not a significant deterrent with many users willing to pay the monthly parking rate even without routinely using the space. This may indicate an insecurity about the reliability of supply with buyers preferring to bear the burden of excess parking cost over the risk insufficient parking.

The zone summaries document findings for each of the quadrants of Downtown as well as the University Corner area. For the purposes of this analysis

Practical capacity is generally between 75% and 85% of the total number of spaces for on- street parking and 95% of off-street spaces. Times when parking demand reached practical capacity are coded light pink in the tables that follow.

Maximum capacity is generally considered to be an occupancy of 86% to 100% of the total number of space either on- or off-street. Periods when parking demand reached or exceeded maximum capacity are coded dark pink in the tables.

Well managed parking will generally approach, but not routinely exceed, the practical capacity.

The Cultural Zone experiences high on-street occupancy for all parking types for much of the weekday. This demand grows during the evening hours. Unlike the other zones surveyed, the Cultural Zone sees even greater demand on Saturdays when the dominant restriction type – a two-hour time limit – exceeds the practical capacity for the entire day and exceeds the maximum capacity during dinner hours. Concurrently during peak periods, the utilization of public off- street lots is far below capacity, never exceeding 61 percent, indicating a comparative under- utilization of these resources (Figures 17 – 20).

Cultural Zone: Weekday

The Cultural Zone has greater than 80 percent occupancy for all on-street parking types for a large majority of the weekday, with demand peaking in the evening hours. Concurrently, unused capacity exists in the off-street facilities.

Unrestricted spaces (along High Street), though limited in quantity, are high in demand, generally filling before restricted spaces and remaining fully occupied for the duration of the day, including evening hours. Turnover of these spaces is low, with each space

serving, on average, just 3.3 vehicles per day compared to roughly 6 vehicles per day served by the time restricted spaces.

One- and two-hour restricted space utilization exceeds the practical capacity for half of the study period. Twenty-seven percent of motorists overstay the one-hour time restriction while 16 percent exceed the two-hour maximum permitted period.

Fifty-nine percent of all vehicles stay less than one hour.

Parking duration in unrestricted spaces was more than double that of time restricted spots (averaging 3.3 hours compared to roughly 1.6 hours in other spaces).

Summary of Weekday Findings

Field observations and data suggest that the parking market in this area is fairly price sensitive. Despite demonstrating a strong need for longer duration parking, users seem to prefer the inconvenience of time limits on free parking over the longer durations, but higher cost, of off- street parking options. Demand spans from morning through the early evening hours, reflective of the 18-hour workforce in this area generated by the mix of office, retail, and food and beverage establishments.

The Cultural Zone demonstrates strong demand for both short-term patron and transactional parking and longer-term employee parking. In general, the existing time-restricted parking appears to meet the needs of shoppers and other patrons to the area.

Figure 17 Downtown Cultural Zone Weekday Utilization Table

Utilization Rates: Downtown Cultural Zone Wednesday, April 22, 2015 (On-Street) – Wednesday, May 13, 2015 (Off-Street) | |||||||

On-Street | Off-Street | ||||||

2 Hour | 1 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | Public Lots | Private Lots | |

Capacity | 145 | 7 | 27 | 40 | 219 | 77-173* | 117-213* |

8 AM | 35% | 100% | 96% | 20% | 42% | ||

9 AM | 72% | 100% | 93% | 55% | 72% | ||

10 AM | 89% | 100% | 100% | 45% | 83% | 49% | 52% |

11 AM | 79% | 71% | 93% | 40% | 74% | ||

12 PM | 88% | 71% | 96% | 58% | 83% | ||

1 PM | 86% | 57% | 100% | 48% | 80% | 94% | 42% |

2 PM | 76% | 71% | 93% | 38% | 71% | ||

3 PM | 84% | 100% | 74% | 65% | 80% | ||

4 PM | 83% | 71% | 89% | 63% | 80% | 56% | 28% |

5 PM | 88% | 86% | 93% | 63% | 84% | ||

6 PM | 92% | 86% | 100% | 80% | 91% | ||

7 PM | 91% | 86% | 100% | 83% | 90% | 36% | 33% |

*Variable capacities reflect the varying operation of the lot at 300 Preston Avenue (Citizens Commonwealth Center) which only allows for tenant/patron parking during normal business hours. The lot functions as publicly available paid parking at all other times.

Figure 18 Downtown Cultural Zone Weekday Turnover Table

On-Street Duration and Turnover Rates: Downtown Cultural Zone Wednesday, April 22, 2015 8:00 AM – 8:00 PM | |||||

2 Hour | 1 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | |

Capacity | 145 | 7 | 27 | 40 | 219 |

Average duration | 1.6 | 1.4 | 3.3 | 1.6 | 1.8 |

Average turnover | 5.7 | 7.0 | 3.3 | 3.9 | 5.1 |

Less than 1 hour | 60% | 73% | 43% | 58% | 59% |

1-2 hours | 24% | 12% | 21% | 27% | 24% |

2-5 hours | 15% | 14% | 12% | 13% | 14% |

5+ hours | 1% | - | 23% | 1% | 3% |

Cultural Zone: Saturday

On-street parking demand remains strong on weekends in the Cultural Zone. Two-hour parking spaces are the first to fill, while other spaces see increasing occupancy throughout the morning. By early afternoon, there is greater than 85 percent occupancy for all parking types. By evening demand exceeds capacity and illegal parking on-street can be readily observed.

Off-street utilization is comparatively low, even in the evening hours during the height of on-street demand. Off-street utilization is far below capacity, never exceeding 50 percent.

Vehicles tend to stay longer on Saturdays than on weekdays, with 43% of vehicles staying less than one hour compared to 59 percent on weekdays. Twenty-six percent of motorists are overstaying the two-hour time restriction in this zone compared to 16% weekdays.

Similarly, turnover is significantly lower on Saturdays than weekdays with two-hour spaces servicing just 4.6 vehicles on Saturdays compared to 5.7 on weekdays and one- hour spaces serving even fewer (3.6 vehicles compared to 7.0 vehicles during the week).

Summary of Saturday Findings

Once again, even on weekends the Cultural Zone demonstrates demand for longer duration parking. This demand is even more pronounced on Saturdays than on weekdays, likely attributable to the destination-district nature of the zone. Despite this demand for longer duration parking, the off-street facilities are poorly used. This may be a result of the pricing imbalance between on- and off-street opportunities, but may also be attributable to poor wayfinding or signage as it is reasonable to conclude that many patrons of the Cultural Zone may be visitors to the city unfamiliar with the location or operation of the off-street facilities.

Figure 19 Downtown Cultural Zone Saturday Utilization Table

Utilization Rates: Downtown Cultural Zone Saturday, May 2, 2015 (On-Street) – Saturday, May 16, 2015 (Off-Street) | |||||||

On-Street | Off-Street | ||||||

2 Hour | 1 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | Public Lots | Private Lots | |

Capacity | 134 | 7 | 26 | 47 | 214 | 173 | 117 |

11 AM | 91% | 57% | 77% | 47% | 79% | ||

12 PM | 89% | 57% | 77% | 49% | 78% | ||

1 PM | 87% | 71% | 77% | 57% | 79% | 31% | 17% |

2 PM | 93% | 71% | 85% | 66% | 85% | ||

3 PM | 96% | 71% | 81% | 68% | 87% | ||

4 PM | 94% | 71% | 88% | 66% | 86% | 23% | 22% |

5 PM | 97% | 57% | 73% | 79% | 89% | ||

6 PM | 101% | 100% | 65% | 83% | 93% | ||

7 PM | 107% | 100% | 77% | 79% | 97% | 45% | 11% |

8 PM | 102% | 86% | 92% | 70% | 93% | ||

9 PM | 99% | 100% | 96% | 64% | 91% | ||

Figure 20 Downtown Cultural Zone Saturday Turnover Table

On-Street Duration and Turnover Rates: Downtown Cultural Zone Saturday, May 2, 2015 11:00 AM – 10:00 PM | |||||

2 Hour | 1 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | |

Capacity | 134 | 7 | 26 | 47 | 214 |

Average duration | 2.2 | 2.4 | 4.3 | 3.0 | 2.5 |

Average turnover | 4.6 | 3.6 | 2.0 | 2.3 | 3.8 |

Less than 1 hour | 47% | 44% | 15% | 37% | 43% |

1-2 hours | 27% | 28% | 30% | 27% | 27% |

2-5 hours | 19% | 24% | 25% | 19% | 19% |

5+ hours | 7% | 4% | 30% | 17% | 10% |

Impacted heavily by the municipal and county uses in the area, the Government Zone sees heavy usage during traditional business hours before a large dropoff in demand in the late afternoon. On-street parking utilization reaches practical capacity by early morning and maintains this level of occupancy until mid-afternoon. Over 13 percent of on-street spaces in this zone are reserved for government employees. These spaces have comparatively lower utilization and turnover rates.

The Market Street garage is the only source of public off-street parking in this zone. In this zone, due to the demands generated by the municipal uses, the garage is well used, commonly achieving utilization slightly above practical capacity at midday (Figures 21 – 22).

On Saturday, occupancy for all on-street parking types is greatly reduced in the Government Zone. This is also a sharp contrast to the neighboring Cultural Zone. Spaces in the Market Street garage are more available on Saturday with utilization below 60 percent (Figures 23 – 24).

Government Zone: Weekday

Higher than 80 percent occupancy for all parking types occurs during the morning hours, with a large dropoff in the late afternoon. It should be noted that curbside occupancy observations were made on a Wednesday; Tuesday mornings are traditionally the busiest day and period for court activities.

Two-hour restricted spaces, which make up more than half of the on-street inventory, see a particular lack of availability during the morning.

The Market Street garage is the only public off-street parking in this zone and has a high midday occupancy, peaking at 87 percent.

Forty-four percent of all vehicles stay less than one hour.

Twenty-seven percent of motorists are overstaying the one-hour time restriction.

Twenty-four percent of motorists are overstaying the two-hour time restriction.

Utilization and turnover of spaces reserved for government use is very low.

Summary of Weekday Findings

Parking is highly used in the Government Zone, particularly during the work day. Both on- and off-street spaces are used to their practical maximum capacity. On-street spaces tend to fill before off-street facilities, however, at midday, both resources are heavily occupied. This may become acute on court days when jury selection is in process.

Despite this apparent parking shortage, the larger Water Street garage, just a 5 minute walk (approximately 1,200 feet) from the court facility, has significant unused capacity during the periods of highest demand in the Government Zone. At the 2 p.m. peak, the 1,100 space Water Street garage is less than 60 percent occupied, leaving over 400 spaces available for use by Government Zone motorists. Although a a modest walk, this facility may become an ever more attractive option on peak days where parking within the zone is heavily used.

The Government Zone appears to be less price sensitive than other zones. This may be because parking vouchers and employee benefits eliminate or substantially mitigate the impact of the parking fee, essentially balancing the cost to park either on-street or off-street.

Figure 21 Downtown Government Zone Weekday Utilization Table

Utilization Rates: Downtown Government Zone Wednesday, April 22, 2015 (On-Street) – Wednesday, May 13, 2015 (Off-Street) | |||||||

On-Street | Off-Street | ||||||

2 Hour | 1 Hour | Government | All Other Restrictions | Total, All Restrictions | Market Street Garage | Private Lots | |

Capacity | 117 | 17 | 28 | 46 | 208 | 473 | 247 |

8 AM | 62% | 41% | 79% | 39% | 57% | 11% | |

9 AM | 92% | 94% | 71% | 57% | 82% | 49% | |

10 AM | 88% | 82% | 64% | 74% | 81% | 67% | 64% |

11 AM | 87% | 88% | 54% | 63% | 77% | 78% | |

12 PM | 84% | 88% | 61% | 41% | 72% | 79% | |

1 PM | 80% | 82% | 61% | 51% | 72% | 87% | 65% |

2 PM | 79% | 88% | 75% | 61% | 75% | 79% | |

3 PM | 61% | 74% | 64% | 30% | 64% | 74% | |

4 PM | 57% | 71% | 50% | 37% | 53% | 70% | 51% |

5 PM | 56% | 59% | 54% | 37% | 52% | 52% | |

6 PM | 74% | 59% | 54% | 37% | 62% | 23% | |

7 PM | 73% | 59% | 43% | 33% | 59% | 23% | 26% |

Figure 22 Downtown Government Zone Weekday Turnover Table

On-Street Duration and Turnover Rates: Downtown Government Zone Wednesday, April 22, 2015 8:00 AM – 8:00PM | |||||

2 Hour | 1 Hour | Government | All Other Restrictions | Total, All Restrictions | |

Capacity | 117 | 17 | 28 | 46 | 208 |

Average duration | 2.0 | 1.7 | 3.3 | 3.1 | 2.2 |

Average turnover | 4.2 | 4.9 | 2.0 | 2.3 | 3.4 |

Less than 1 hour | 41% | 72% | 29% | 41% | 44% |

1-2 hours | 35% | 7% | 14% | 18% | 28% |

2-5 hours | 23% | 18% | 36% | 23% | 23% |

5+ hours | 1% | 2% | 21% | 17% | 5% |

Government Zone: Saturday

In the Government Zone, occupancy for all parking types is greatly reduced compared with the neighboring Cultural Zone. Even at its peak (8 p.m.), occupancy does not exceed 66 percent.

Two-hour and government restricted spaces are the most well used on Saturdays, with steady occupancy between 60% and 75% from early afternoon through evening. However, even this is well below full occupancy.

The Market Street garage has abundant availability on Saturday. It is most highly occupied in the evening, but even then never higher than 60 percent.

Thirty-four percent of all vehicles are staying less than one hour (compared to 44% weekdays).

Forty-nine percent of motorists are overstaying the one-hour time restriction in this zone (27% weekdays).

Forty-four percent of motorists are overstaying the two-hour time restriction in this zone (24% weekdays).

Turnover is very low with most spaces serving, on average, just two vehicles per day.

Summary of Saturday Findings

Demand is generally low in the Government Zone. Although immediately adjacent to the high- Saturday demand Cultural Zone, there is limited spillover and it does not penetrate all the way over to the Market Street garage. There is a demand for longer duration parking in this zone, but at present it does not appear that there is a need to manage parking supply with either time limits or parking fees in this zone given the modest demand.

This zone could lend itself well to serving as a supplemental resource to the Cultural Zone to meet the demand for longer duration and lower cost parking on Saturdays.

Figure 23 Downtown Government Zone Saturday Utilization Table

Utilization Rates: Downtown Government Zone Saturday, May 2, 2015 (On-Street) – Saturday, May 16, 2015 (Off-Street) | |||||||

On-Street | Off-Street | ||||||

2 Hour | 1 Hour | Government | All Other Restrictions | Total, All Restrictions | Market Street Garage | Private Lots | |

Capacity | 117 | 17 | 28 | 46 | 208 | 473 | 247 |

11 AM | 63% | 71% | 61% | 41% | 59% | 7% | |

12 PM | 68% | 47% | 61% | 41% | 60% | 7% | |

1 PM | 68% | 47% | 57% | 33% | 57% | 8% | 28% |

2 PM | 46% | 47% | 50% | 24% | 42% | 12% | |

3 PM | 59% | 41% | 64% | 28% | 51% | 16% | |

4 PM | 61% | 29% | 68% | 28% | 52% | 16% | 25% |

5 PM | 62% | 35% | 71% | 28% | 53% | 17% | |

6 PM | 61% | 59% | 71% | 35% | 56% | 26% | |

7 PM | 70% | 65% | 57% | 37% | 61% | 41% | 24% |

8 PM | 74% | 71% | 71% | 39% | 66% | 54% | |

9 PM | 72% | 71% | 68% | 41% | 64% | 59% | |

Figure 24 Downtown Government Zone Saturday Turnover Table

On-Street Duration and Turnover Rates: Downtown Government Zone Saturday, May 2, 2015 11:00 AM – 10:00 PM | |||||

2 Hour | 1 Hour | Government | All Other Restrictions | Total, All Restrictions | |

Capacity | 117 | 17 | 28 | 46 | 208 |

Average duration | 2.7 | 1.9 | 4.3 | 2.9 | 2.8 |

Average turnover | 2.6 | 3.1 | 1.6 | 1.3 | 2.2 |

Less than 1 hour | 33% | 51% | 22% | 34% | 34% |

1-2 hours | 24% | 25% | 28% | 14% | 23% |

2-5 hours | 34% | 23% | 24% | 41% | 32% |

5+ hours | 10% | 2% | 26% | 12% | 11% |

The Market Zone in the southwest corner of downtown demonstrates a split personality. During the week, it is a traditional employment and main street retail zone. On Saturdays, the City Market makes it a popular destination district (Figures 25 – 28).

Like other areas with substantial daytime employment and commercial activity, parking demand in the Market Zone is highest in the morning and early afternoon and begins to diminish as the day goes on. Unlike the Cultural Zone, there is limited evening parking demand in the Market Zone during weekday evenings. While free on-street parking is well used, the paid off-street lots are generally only half to two-thirds full even during the peak hour, again demonstrating the impact of pricing on parking demand.

On Saturdays, the zone experiences its most acute supply shortages during the Saturday morning Charlottesville City Market, which inspires its name. The market itself is held on a public surface lot, which drastically reduces capacity while simultaneously generating demand. Although filling the remaining on- and off-street surface parking within the zone to practical capacity, the Water Street garage, located just across the zone boundary to the east, remains no more than 51 percent occupied with more than 500 spaces typically available. Similarly, on Saturday evenings, while the surface lots are generally fully occupied, the Water Street garage is very lightly used.

Market Zone: Weekday

Two-hour restricted (100 spaces) or unrestricted (82) spaces make up the majority of curbside parking in the Market Zone (83%).

Unrestricted spaces reach their practical capacity early in the morning and experience sustained demand throughout the work day. Demand eases substantially after 4 p.m.

Heavily utilized unrestricted parking is in immediate proximity to the two-hour restricted spaces. As a result, two-hour spaces do not see as high a level of utilization, though they do reach practical capacity during business hours.

The few one-hour spaces are very heavily used while generally less than half of the other restricted spaces (most parking for persons with disabilities or loading zones) are used.

Public lot utilization never exceeds 50 percent, roughly 150 spaces are routinely available.

There are very long average stays despite the time restrictions. Only 13% of all vehicles are staying less than one hour. Thirty-six percent of all vehicles stay more than five hours.

Ninety-four percent of motorists are overstaying the one-hour time restriction.

Forty-nine percent of motorists are overstaying the two-hour time restriction in this zone.

Summary of Weekday Findings

While still substantial, the Market Zone has lower typical demand than other zones in the Downtown. Demand is generally for longer duration and is not well matched to the existing time restricted spaces. Off-street parking is significantly underutilized in this zone. Together – the greater willingness to exceed time regulations and the limited usage of paid off-street facilities – may be an indication of more limited enforcement activity compared to other zones. Motorists are more willing to risk an occasional ticket in this zone than routinely pay for parking.

In general, the one-hour restricted parking spaces appear to not serve their intended purpose. These spaces are routinely occupied, but often by drivers that exceed the allowable time limit. At the same time, “Other Restricted” spaces (typically ADA parking or commercial loading) are substantially underutilized. This is an indication to reevaluate both parking categories to examine opportunities to optimize all available curbside spaces during periods of strong demand.

Figure 25 Downtown Market Zone Weekday Utilization Table

Utilization Rates: Downtown Market Zone Thursday, April 23, 2015 (On-Street) – Wednesday, May 13, 2015 (Off-Street) | |||||||

On-Street | Off-Street | ||||||

2 Hour | 1 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | Public Lots | Private Lots | |

Capacity | 100 | 7 | 82 | 29 | 218 | 267 | 433 |

8 AM | 79% | 114% | 94% | 48% | 82% | 11% | 38% |

9 AM | 77% | 100% | 94% | 45% | 80% | ||

10 AM | 77% | 100% | 94% | 45% | 80% | ||

11 AM | 77% | 71% | 94% | 48% | 79% | 42% | 72% |

12 PM | 78% | 71% | 95% | 48% | 80% | ||

1 PM | 78% | 71% | 95% | 55% | 81% | ||

2 PM | 66% | 100% | 85% | 55% | 73% | 43% | 57% |

3 PM | 67% | 86% | 85% | 55% | 73% | ||

4 PM | 76% | 100% | 71% | 48% | 71% | ||

5 PM | 69% | 100% | 72% | 45% | 68% | 45% | 45% |

6 PM | 45% | 100% | 60% | 31% | 50% | ||

7 PM | 53% | 114% | 68% | 45% | 60% | ||

Figure 26 Downtown Market Zone Weekday Turnover Table

On-Street Duration and Turnover Rates: Downtown Market Zone Wednesday, April 22, 2015 8:00 AM – 8:00 PM | |||||

2 Hour | 1 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | |

Capacity | 100 | 7 | 82 | 29 | 218 |

Average duration | 3.7 | 2.5 | 5.0 | 6.9 | 4.3 |

Average turnover | 2.3 | 4.4 | 2.0 | 0.8 | 2.0 |

Less than 1 hour | 15% | 6% | 11% | 17% | 13% |

1-2 hours | 36% | 52% | 25% | 4% | 32% |

2-5 hours | 18% | 42% | 19% | 8% | 20% |

5+ hours | 31% | - | 45% | 71% | 36% |

Market Zone: Saturday

The Market Zone sees utilization of unrestricted spaces that exceeds practical capacity during market hours and again during the evening.

Two-hour spaces see surges in utilization at similar times, but again in lower proportion than immediately adjacent unrestricted spaces.

Public surface lot utilization reaches maximum capacity during market hours due to the loss of significant capacity resulting from the market operation. Public lot utilization exceeds practical capacity during the evening peak.

Average duration of stays is significantly shorter on Saturdays than on weekdays.

Summary of Saturday Findings

Saturday parking demand is high, but not excessive, in this zone. Saturday mornings in the Market Zone are the only time and location that off-street parking utilization exceeds on-street parking. Demand is predictably highest closest to the city market during the morning event.

Demand tapers off midday and begins to rise again on Saturday evenings in association with the dining and entertainment uses in the zone. Parking durations are shorter on weekends, with most users averaging stays of approximately three hours.

Off-street parking on the public surface lot is high in this zone. This lot is contemplated for future development, which would both reduce the public parking supply and relocate parking to a garage facility. Existing demand, save for during the active market time, is less than supply. Private lots in the immediate zone have abundant excess capacity capable of absorbing any demand unmet in the public lots if sharing arrangements were made.

Figure 27 Downtown Market Zone Saturday Utilization Table

Utilization Rates: Downtown Market Zone Saturday, May 2, 2015 (On-Street) – Saturday, May 16, 2015 (Off-Street) | |||||||

On-Street | Off-Street | ||||||

2 Hour | 1 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | Public Lots | Private Lots | |

Capacity | 99-105* | 7 | 82 | 33 | 221-227* | 105-267* | 433 |

11 AM | 88% | 100% | 95% | 42% | 84% | 100% | 45% |

12 PM | 63% | 100% | 85% | 36% | 68% | ||

1 PM | 45% | 100% | 70% | 30% | 54% | ||

2 PM | 43% | 100% | 65% | 30% | 51% | 34% | 21% |

3 PM | 54% | 100% | 40% | 42% | 49% | ||

4 PM | 52% | 100% | 40% | 39% | 48% | ||

5 PM | 70% | 71% | 46% | 52% | 59% | 53% | 19% |

6 PM | 70% | 71% | 46% | 48% | 59% | ||

7 PM | 80% | 100% | 88% | 64% | 81% | ||

8 PM | 79% | 100% | 88% | 55% | 79% | 87% | 15% |

9 PM | 65% | 100% | 87% | 45% | 71% | ||

Figure 28 Downtown Market Zone Saturday Turnover Table

On-Street Duration and Turnover Rates: Downtown Market Zone Saturday, May 2, 2015 11:00 AM – 10:00 PM | |||||

2 Hour | 1 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | |

Capacity | 99-105* | 7 | 82 | 33 | 221-227* |

Average duration | 2.8 | 2.4 | 3.3 | 3.6 | 3.0 |

Average turnover | 2.4 | 4.3 | 2.3 | 1.3 | 2.3 |

Less than 1 hour | 19% | 20% | 11% | 23% | 17% |

1-2 hours | 41% | 40% | 27% | 36% | 35% |

2-5 hours | 34% | 40% | 52% | 23% | 40% |

5+ hours | 7% | - | 10% | 18% | 8% |

*Variable capacities reflect that certain on-street and off-street spaces were unavailable during the operation and tear- down time of the Charlottesville City Market. The market is held on a public off-street lot, completely precluding parking.

The Southeast Zone is dominated by unrestricted curbside parking. Located along the southern and southeastern edges of the downtown study area, this area constitutes 28 percent of the total on-street parking inventory in the downtown and 79 percent in this zone. The unrestricted nature leads to very low turnover conditions in the Southeast Zone. Weekday demand is steady and high but is not excessive in this zone. Despite its proximity to downtown destinations, the Water Street garage retains a large amount of excess capacity; there are always more than 375 empty spaces (Figures 29 – 30).

The weekend conditions are exactly opposite in this zone. Unrestricted spaces, especially those in low accessibility areas, go unused while the prime two-hour spaces see high utilization after restrictions have expired. The Water Street garage remains only partially occupied throughout the day on Saturdays as it is on weekdays (Figures 31 – 32).

Southeast Zone: Weekday

The majority of on-street parking in the Southeast Zone is unrestricted – 278 spaces, accounting for 79 percent of the total curbside space.

These unregulated spaces are highly utilized (88%) during the peak of the traditional work day (9 a.m. to 4 p.m.). This free, long duration, and unrestricted on-street parking is generally preferred over the paid structured parking in the Water Street garage.

The 1,019-space Water Street Garage peaks at 62% occupancy at 1 p.m., generally leaving more than 400 parking spaces unused.

The 54 two-hour restricted spaces are not fully used at any point during the day; however they see their greatest period of use during the lunch hour.

Only 20 percent of all vehicles are staying less than one hour, with most users averaging a stay of five hours or longer.

Thirty-five percent of motorists are overstaying the two-hour time restriction in this zone.

Summary of Weekday Findings

The field observations and review of data indicate that again the imbalance in price between the paid parking garage and the free on-street spaces motivate most drivers to make the economical

choice to park for free. Given the general lack of time restrictions in this zone, on-street parking readily meets the need of all-day, workforce parking. As a result, the city investment in the municipal garage is not presently optimized.

Although demand for the unregulated spaces routinely threatens to exceed supply, utilization of nearby two-hour restricted spaces remains significantly lower. The motorists who do park in these spaces most likely include a significant share of spillover users unable to find an available unrestricted space that day as evidenced by the trend of over-staying the two-hour restriction.

As in other zones, the “other restricted” spaces rarely reach capacity. However, utilization in the Southeast Zone increases in the afternoon hours even while demand declines for all other spaces.

Figure 29 Downtown Southeast Zone Weekday Utilization Table

Utilization Rates: Downtown Southeast Zone Thursday, April 23, 2015 (On-Street) – Wednesday, May 13, 2015 (Off-Street) | ||||||

On-Street | Off-Street | |||||

2 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | Water Street Garage | Private Lots | |

Capacity | 54 | 278 | 22 | 354 | 1019 | 550 |

8 AM | 22% | 21% | 36% | 22% | 11% | |

9 AM | 65% | 91% | 41% | 84% | 42% | 43% |

10 AM | 72% | 91% | 50% | 86% | 54% | |

11 AM | 80% | 88% | 41% | 84% | 58% | |

12 PM | 83% | 96% | 59% | 92% | 60% | 44% |

1 PM | 80% | 97% | 45% | 91% | 62% | |

2 PM | 70% | 93% | 68% | 88% | 61% | |

3 PM | 61% | 93% | 50% | 85% | 58% | 47% |

4 PM | 43% | 57% | 41% | 54% | 55% | |

5 PM | 30% | 59% | 55% | 54% | 45% | |

6 PM | 69% | 59% | 73% | 61% | 22% | 34% |

7 PM | 69% | 46% | 95% | 53% | 21% | |

Figure 30 Downtown Southeast Zone Weekday Turnover Table

On-Street Duration and Turnover Rates: Downtown Southeast Zone Wednesday, April 22, 2015 8:00 AM – 8:00 PM | ||||

2 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | |

Capacity | 54 | 278 | 22 | 354 |

Average duration | 2.9 | 6.1 | 3.0 | 5.1 |

Average turnover | 2.6 | 1.4 | 2.0 | 1.6 |

Less than 1 hour | 35% | 12% | 49% | 20% |

1-2 hours | 30% | 9% | 18% | 15% |

2-5 hours | 19% | 23% | 18% | 22% |

5+ hours | 16% | 56% | 16% | 43% |

Southeast Zone: Saturday

The unrestricted parking in the Southeast Zone is significantly less utilized on Saturdays than it is on weekdays. Demand is highest in the morning and generally declines over the course of the day, but is never greater than two-thirds occupied. Large numbers of spaces on Avon Street near and under the 9th Street flyover go completely unused for the entire day.

The Water Street garage is generally never more than half full on Saturdays. It peaks in occupancy during market hours (owing to its location on the boundary between zones) and in the evening hours.

The two-hour restricted spaces closest to downtown attractions reach practical capacity immediately before the restriction is set to expire at 6 p.m. and remain heavily utilized throughout the evening.

Seventy-six percent of all vehicles stay more than one hour and 53 percent of all vehicles stay more than two hours. Only a small percentage (14%) stay for five hours or more on Saturdays.

Summary of Saturday Findings

On Saturdays, the Southeast Zone is generally a parking spillover zone for the Market and Cultural Zones of downtown. Areas proximate to Main Street have a fair amount of demand while other areas go fully unused. The Water Street garage, although available and accessible to downtown destinations, remains underutilized as motorists opt for the readily available on-street spaces. Given evidence of current demands, the existing two-hour restrictions are generally doing an effective job of managing Saturday demands while still encouraging a sufficient amount of turnover. Abundant options are available for any motorist requiring parking accommodation in excess of two hours.

Both the unregulated spaces and the Market Street garage may be untapped opportunities to accommodate weekend workforce needs or patrons of the downtown entertainment venues.

Figure 31 Downtown Southeast Zone Saturday Utilization Table

Utilization Rates: Downtown Southeast Zone Saturday, May 2, 2015 (On-Street) – Saturday, May 16, 2015 (Off-Street) | ||||||

On-Street | Off-Street | |||||

2 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | Water Street Garage | Private Lots | |

Capacity | 54 | 278 | 22 | 354 | 1019 | 550 |

11 AM | 83% | 66% | 36% | 67% | 33% | |

12 PM | 67% | 52% | 45% | 54% | 44% | 30% |

1 PM | 50% | 49% | 36% | 48% | 34% | |

2 PM | 57% | 43% | 45% | 45% | 29% | |

3 PM | 59% | 34% | 45% | 38% | 22% | 28% |

4 PM | 72% | 28% | 45% | 36% | 19% | |

5 PM | 85% | 38% | 45% | 46% | 11% | |

6 PM | 85% | 44% | 45% | 50% | 20% | 29% |

7 PM | 74% | 44% | 50% | 49% | 35% | |

8 PM | 87% | 45% | 59% | 52% | 46% | |

9 PM | 87% | 43% | 50% | 50% | 51% | 34% |

Figure 32 Downtown Southeast Zone Saturday Turnover Table

On-Street Duration and Turnover Rates: Downtown Southeast Zone Saturday, May 2, 2015 11:00 AM – 10:00 PM | ||||

2 Hour | Unrestricted | All Other Restrictions | Total, All Restrictions | |

Capacity | 54 | 278 | 22 | 354 |

Average duration | 2.7 | 3.4 | 3.6 | 3.3 |

Average turnover | 3.0 | 1.4 | 1.3 | 1.6 |

Less than 1 hour | 31% | 22% | 21% | 24% |

1-2 hours | 30% | 20% | 28% | 23% |

2-5 hours | 29% | 44% | 31% | 39% |

5+ hours | 11% | 14% | 21% | 14% |

The University Corner study area has an entirely different parking dynamic on both weekdays and weekends. Long stays, on the order of seven to nine hours, dominate the use of the unrestricted spaces, which make up roughly half of the inventory. Occupancy of these unrestricted spaces never dips below 93 percent. Combining all restrictions, space availability is particularly constrained from 9 a.m. to 4 p.m. on weekdays and on Saturday evenings (Figures 33 – 36).

University Zone: Weekday (school year)

The University Corner study area has an overall occupancy of 85 percent or greater at all times of day. Demand begins early and remains consistently high throughout the day.

Over half the curbside parking supply in the University Corner Zone is unrestricted.

Permit parking exceeds supply, indicating that there are potentially more vehicles permitted than the curbside space of the permit zone can accommodate.

Even “other restriction” spaces approach or meet their practical utilization capacity. This does not occur in any other zone studied.

Over one third of all vehicles are staying more than five hours.

Average duration of unrestricted stays is greater than seven hours.

Summary of Weekday Findings

Parking demand is consistently high throughout the University Corner area. Although a comparatively small number of spaces are intended for commercial patron use – the 46 two-hour restricted spaces representing less than a quarter of the zone supply – these spaces do not appear to be used by visitors or patrons. These spaces appear to be utilized by persons affiliated with the university (students, staff, researchers, etc.) and occupied for a longer period of time. It is unclear where or how the short-term parkers are accommodated in the zone. Given the evidence that demand routinely exceeds supply, the University Corner area may benefit substantially from a

demand-responsive pricing system to ensure that at least a small number of parking spaces are reliably available for patrons and visitors needing to access the University Corner district.

Figure 33 University Zone Weekday Utilization Table

On-Street Utilization Rates: University Corner Study Area Thursday, April 23, 2015 | |||||

2 Hour | Permit | Unrestricted | All Other Restrictions | Total, All Restrictions | |

Capacity | 46 | 31 | 97 | 22 | 196 |

8 AM | 85% | 90% | 100% | 41% | 88% |

9 AM | 87% | 87% | 98% | 68% | 90% |

10 AM | 80% | 100% | 98% | 77% | 92% |

11 AM | 87% | 103% | 98% | 73% | 93% |

12 PM | 91% | 100% | 98% | 55% | 92% |

1 PM | 96% | 87% | 96% | 77% | 92% |

2 PM | 89% | 94% | 97% | 82% | 93% |

3 PM | 89% | 97% | 97% | 64% | 91% |

4 PM | 83% | 90% | 97% | 64% | 89% |

5 PM | 80% | 81% | 93% | 64% | 85% |

6 PM | 89% | 84% | 94% | 68% | 88% |

7 PM | 91% | 94% | 95% | 27% | 86% |

Figure 34 University Zone Weekday Turnover Table

On-Street Duration and Turnover Rates: University Corner Study Area Thursday, April 23, 2015 8:00 AM – 8:00 PM | |||||

2 Hour | Permit | Unrestricted | All Other Restrictions | Total, All Restrictions | |

Capacity | 46 | 31 | 97 | 22 | 196 |

Average duration | 3.7 | 6.6 | 7.1 | 2.0 | 5.0 |

Average turnover | 2.7 | 1.6 | 1.6 | 3.6 | 2.1 |

Less than 1 hour | 25% | 20% | 8% | 65% | 26% |

1-2 hours | 21% | 10% | 8% | 14% | 14% |

2-5 hours | 32% | 18% | 24% | 14% | 23% |

5+ hours | 22% | 53% | 60% | 8% | 37% |

University Zone: Saturday (school year)

While demand remains substantial throughout the day, particularly for the unrestricted spaces, demand increases during evening hours when it exceeds 90% in the two-hour restricted spaces.

Forty percent of all vehicles are staying more than five hours.

Average duration of unrestricted stays is nine hours.

Summary of Saturday Findings

As it is on weekdays, parking demand is consistently high throughout the University Corner area on weekends. The unrestricted spaces exceed maximum practical occupancy throughout the day. It is expected that instances of illegal parking or circling to look for parking is common as a result. Permit parking too remains high. Two-hour parking is lower during the day on Saturday but increases in the evening.

Given the high demand throughout the area and across restriction types, pricing tools, in combination with transportation demand management benefits, are expected to be the most effective management strategy for this area. The market-based approach of managing scarce goods through pricing may extend to the permit parking areas as well where pricing may manage the demand for permits such that a permit may indicate a realistic expectation of parking availability as opposed to simply being a “license to fish.”

Figure 35 University Zone Saturday Utilization Table

On-Street Utilization Rates: University Corner Study Area Saturday, April 25, 2015 | |||||

2 Hour | Permit | Unrestricted | All Other Restrictions | Total, All Restrictions | |

Capacity | 46 | 31 | 97 | 22 | 196 |

10 AM | 67% | 84% | 98% | 45% | 83% |

11 AM | 80% | 87% | 97% | 77% | 89% |

12 PM | 78% | 87% | 97% | 64% | 87% |

1 PM | 74% | 77% | 97% | 82% | 87% |

2 PM | 78% | 77% | 99% | 64% | 87% |

3 PM | 74% | 81% | 99% | 32% | 83% |

4 PM | 76% | 90% | 97% | 59% | 87% |

5 PM | 87% | 94% | 101% | 50% | 91% |

6 PM | 93% | 94% | 99% | 59% | 92% |

7 PM | 93% | 100% | 99% | 50% | 92% |

8 PM | 100% | 100% | 97% | 55% | 93% |

9 PM | 96% | 100% | 99% | 36% | 91% |

Figure 36 University Zone Saturday Turnover Table

On-Street Duration and Turnover Rates: University Corner Study Area Saturday, April 25, 2015 10:00 AM – 10:00 PM | |||||

2 Hour | Permit | Unrestricted | All Other Restrictions | Total, All Restrictions | |

Capacity | 46 | 31 | 97 | 22 | 196 |

Average duration | 3.5 | 7.7 | 9.0 | 1.6 | 5.4 |

Average turnover | 2.7 | 1.4 | 1.3 | 4.0 | 1.9 |

Less than 1 hour | 46% | 9% | 11% | 80% | 38% |

1-2 hours | 16% | 7% | 4% | 9% | 9% |

2-5 hours | 15% | 21% | 10% | 7% | 12% |

5+ hours | 23% | 63% | 75% | 4% | 40% |

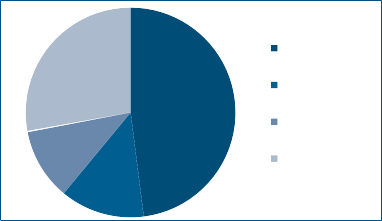

While the majority of on- street parking in the study area is time limited (560 of the 1,001 parking spaces), generally to two hours, these limits are rarely enforced.

Through the first quarter of 2015, the City of Charlottesville issued 4,666 tickets citywide, totaling

11%

$105,070 in fines: 1,656 tickets were issued in January ($35,105), 1,269 in February ($29,285), and 1,741 in March ($40,680).

On average, enforcement

Overtime

28%

Expired Meter

48%

Figure 37 Parking Violation January - March 2015

Permit zone w/o

Permit

Other

13%

officers issued 25 tickets per day (over the quarter) in the downtown and 10 tickets per day in the University Corner area.